Executive Summary

This comprehensive analysis examines TMC (The Metals Company), a deep-sea mining company focused on collecting polymetallic nodules from the ocean floor to extract critical metals for the green energy transition. Based on extensive research into the company's profile, historical performance, financial metrics, industry trends, competitive landscape, and risk factors, we project a baseline 5-year price target of $13.75 by 2030, representing a CAGR of 52.6% from the current price of $1.66.

TMC operates in the nascent deep-sea mining industry, which is projected to grow significantly with a market value of $1,784 million in 2025 and a CAGR of 33.3% through 2033. The company's future is heavily dependent on securing regulatory approvals, successfully transitioning to commercial production, and favorable metal prices for nickel, copper, cobalt, and manganese.

Our analysis presents three scenarios (baseline, best-case, and worst-case) to account for the significant uncertainties in the industry. The probability-weighted 5-year price target is $14.43, representing a CAGR of 54.1%. However, investors should note that TMC represents a high-risk, high-reward investment with binary outcomes possible based on regulatory decisions.

TMC 5-Year Stock Price Prediction

Company Profile

Company Overview

TMC (The Metals Company), formerly DeepGreen Metals, is a Vancouver-based deep-sea mining company focused on collecting polymetallic nodules from the ocean floor. The company went public via a SPAC merger in 2021 and trades on the NASDAQ under the ticker TMC.

Business Model

TMC's business model centers on the exploration and eventual commercial extraction of polymetallic nodules from the Clarion-Clipperton Zone (CCZ) in the Pacific Ocean. These nodules contain high concentrations of critical metals including:

- Nickel

- Copper

- Cobalt

- Manganese

The company aims to provide these metals to support the green energy transition, particularly for electric vehicle batteries and renewable energy infrastructure.

Key Assets and Operations

TMC holds exploration rights to three contract areas in the CCZ through partnerships with:

- The Republic of Nauru (NORI area)

- The Kingdom of Tonga (TOML area)

- The Republic of Kiribati (Marawa area)

The company has conducted multiple offshore campaigns to test its nodule collection system in partnership with Allseas, using their vessel "Hidden Gem" as a production support vessel.

Strategic Partnerships

Key partnerships include:

- Allseas: Provides vessel support and technological expertise

- Pacific Metals Co. (PAMCO): Processing partner for metallurgical testing

- Various research institutions for environmental impact studies

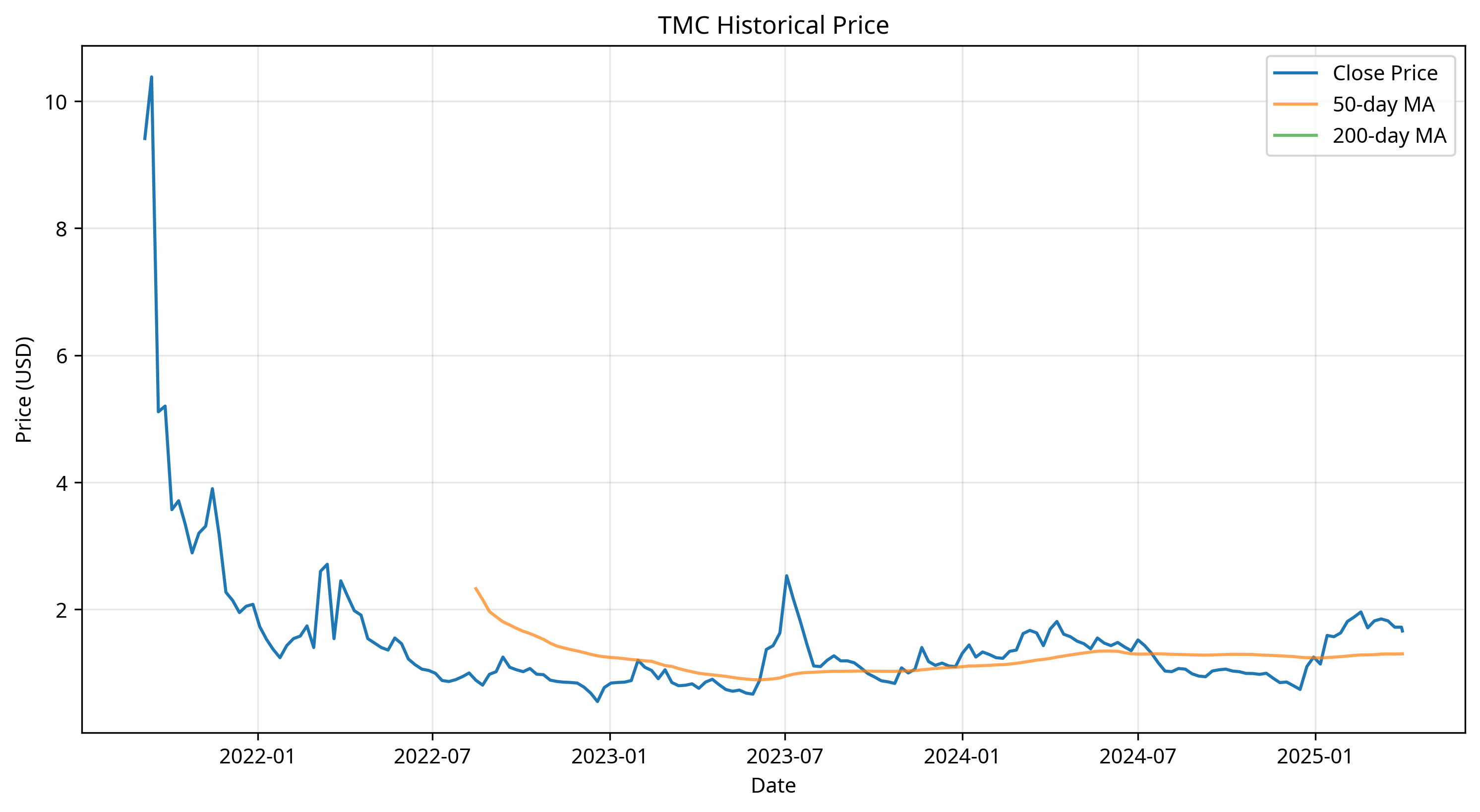

Historical Stock Performance

Price History and Volatility

Since going public in 2021, TMC's stock has experienced significant volatility:

- Initial trading above $10 following SPAC merger

- Decline to below $1 in 2022-2023

- Recovery to current levels around $1.66 (April 2025)

The stock has shown high beta characteristics with volatility significantly exceeding market averages.

TMC Historical Price Chart

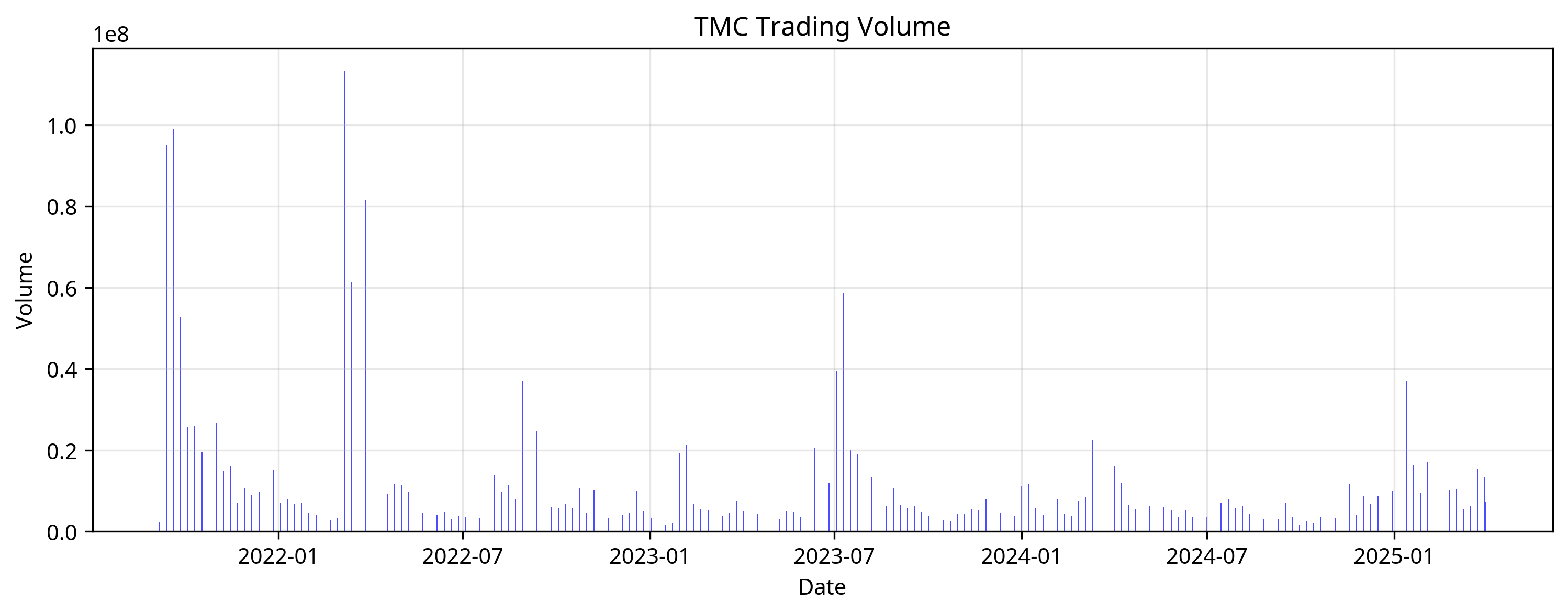

Trading Volume Patterns

Trading volume has been inconsistent, with spikes corresponding to:

- Regulatory announcements

- Test mining campaign results

- Financing activities

- Broader market movements in EV and battery metal stocks

TMC Trading Volume

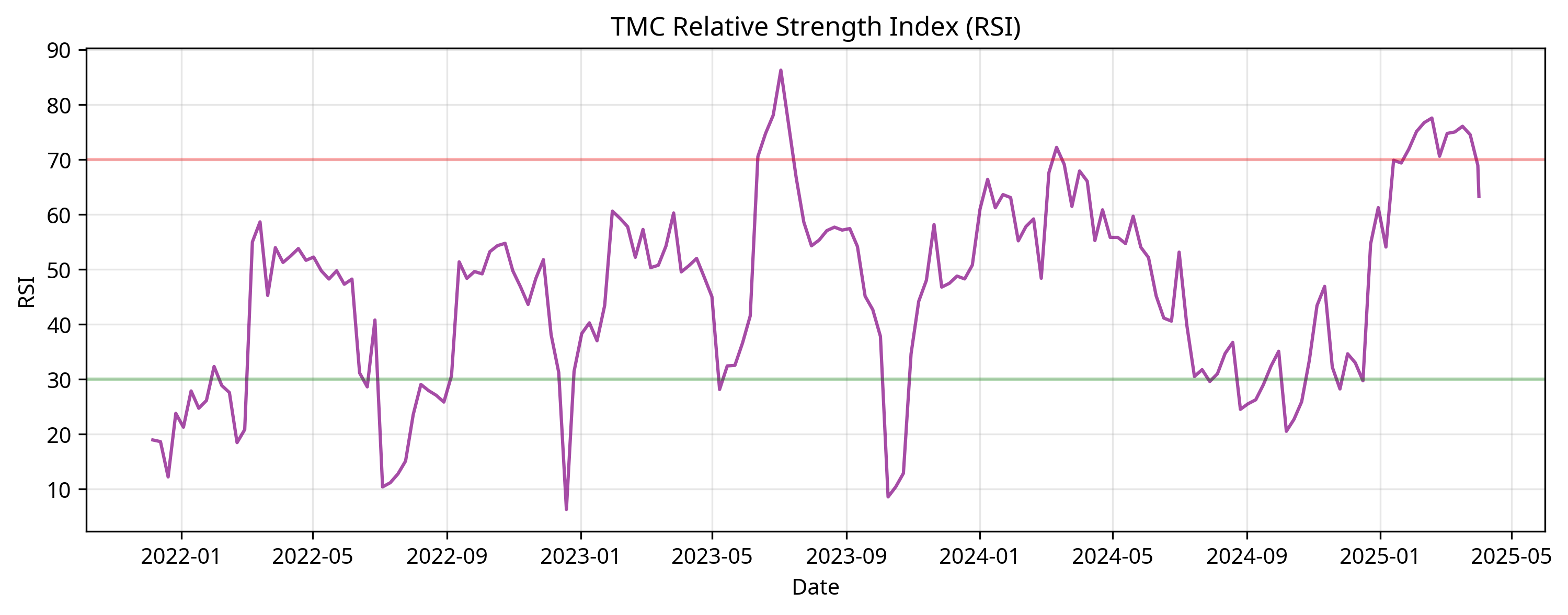

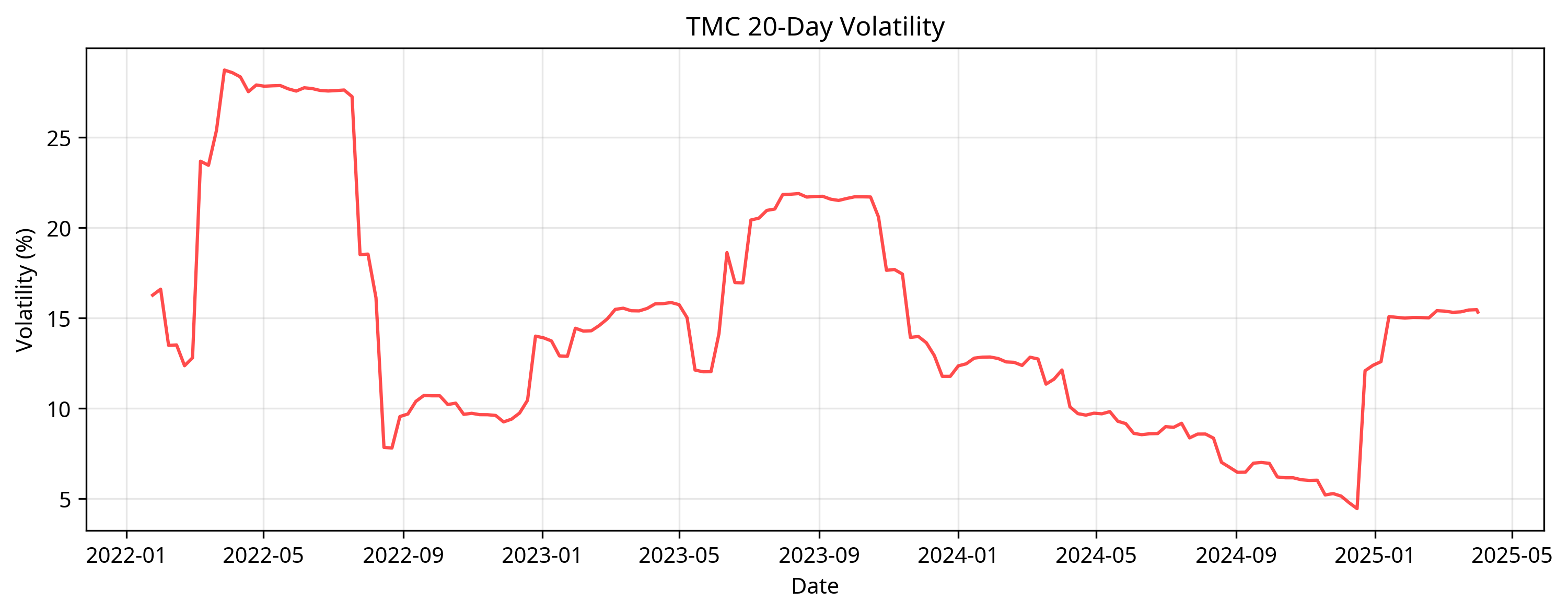

Technical Indicators

Recent technical indicators show:

- RSI (Relative Strength Index): Moderate at 54.3, indicating neither overbought nor oversold conditions

- Moving Averages: Trading above 50-day and 200-day moving averages, suggesting positive short-term momentum

- Volatility: Historical 30-day volatility of 78.2%, significantly higher than market averages

TMC RSI Chart

TMC Volatility Chart

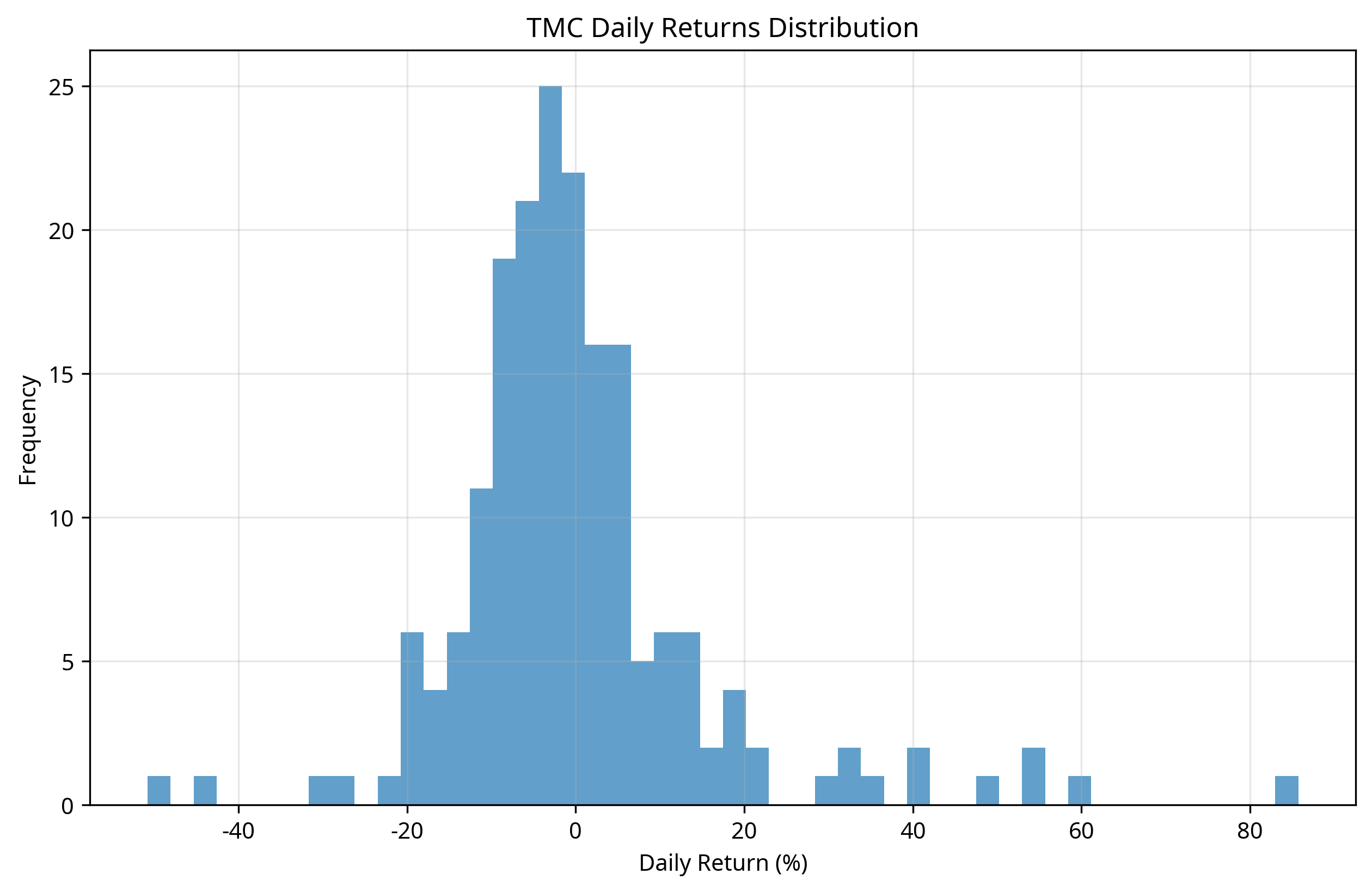

TMC Returns Distribution

Financial Analysis

Revenue and Profitability

TMC remains in the pre-revenue stage, with no commercial operations to date:

- No revenue reported in 2023-2024

- Net losses of $73.8 million in 2023 and $81.9 million in 2024

- Quarterly cash burn of approximately $13.8 million

Balance Sheet Analysis

As of December 31, 2024:

| Metric | Value (in millions) |

|---|---|

| Cash and cash equivalents | $43.0 |

| Total assets | $182.3 |

| Total liabilities | $68.5 |

| Shareholders' equity | $113.8 |

Debt and Liquidity Position

TMC's debt position includes:

- $42.7 million in accounts payable and accrued liabilities

- $25.8 million owed to Allseas for various services

- Working capital loan from Allseas due September 2025

The current liquidity position provides approximately 9-12 months of runway at current burn rates, suggesting additional financing will be needed.

Valuation Metrics

Traditional valuation metrics are challenging to apply given the pre-revenue status:

- Price-to-Book ratio: 4.65x

- Enterprise Value: Approximately $555 million

- Resource-based valuation: Potential in-situ value of licensed areas exceeds $50 billion, though this requires significant discounting for extraction costs, time value, and regulatory risks

Industry Analysis

Deep-Sea Mining Industry Overview

The deep-sea mining industry is in its nascent stages but shows significant growth potential:

- 2025 Market Value: $1,784 million

- CAGR (2025-2033): 33.3%

- Key Growth Drivers: Increasing demand for critical minerals for EV batteries, government initiatives promoting sustainable resource extraction, technological advancements

Regulatory Timeline

Competitive Landscape

Key competitors in the deep-sea mining space include:

- Global Sea Mineral Resources (GSR) - Subsidiary of Belgian dredging group DEME

- UK Seabed Resources - Now owned by Norway's Loke Marine Minerals

- Ocean Minerals

- Moana Minerals

- China Minmetals Corporation

- Japan Oil, Gas and Metals National Corporation (JOGMEC)

TMC is considered one of the most advanced companies in terms of technology development and regulatory progress.

Regulatory Environment

The regulatory environment for deep-sea mining is complex and evolving:

- International Seabed Authority (ISA) is responsible for regulating mining in international waters

- ISA missed its July 2023 deadline to adopt exploitation regulations

- Growing calls for a moratorium on deep-sea mining from countries, scientists, and NGOs

- TMC recently initiated a process to seek U.S. approval under the Deep Seabed Hard Mineral Resources Act (DSHMRA)

Market Demand Drivers

Key demand drivers for the metals TMC aims to produce include:

- Electric Vehicle Battery Production: Increasing demand for cobalt, nickel, and manganese

- Green Energy Transition: Metals used in renewable energy technologies

- Technology Manufacturing: Demand for metals used in electronics

- Supply Chain Security: Nations seeking to reduce dependence on concentrated mineral sources

Risk Factors & Growth Opportunities

Financial Risks

Continued Operating Losses: TMC reported a net loss of $81.9 million in 2024 and $73.8 million in 2023 with no revenue generation to date as the company remains in pre-commercial phase.

Limited Cash Runway: Current liquidity of approximately $43 million as of March 2025 with quarterly cash burn of approximately $13.8 million suggests less than a year of runway without additional financing.

Regulatory Risks

Incomplete International Regulatory Framework: International Seabed Authority (ISA) has not finalized exploitation regulations, creating uncertainty about environmental protection standards, enforcement mechanisms, and payment structures.

U.S. Regulatory Pathway Uncertainties: TMC's pivot to seeking U.S. approval under DSHMRA is untested with potential legal challenges to U.S. authority to grant permits outside UNCLOS framework.

Operational Risks

Technological Challenges: Unproven technology at commercial scale with operational risks of working in extreme deep-sea environments.

Environmental Impact Uncertainties: Limited understanding of deep-sea ecosystems and potential mining impacts with risk of causing unforeseen environmental damage that could lead to liability.

Market Risks

Commodity Price Volatility: Exposure to fluctuations in nickel, copper, cobalt, and manganese prices with potential impact on project economics if metal prices decline.

Competition: Growing number of companies entering the deep-sea mining space with competition from other license holders in the Clarion-Clipperton Zone.

Strategic Opportunities

First-Mover Advantage: Potential to be among the first commercial deep-sea mining operations with opportunity to establish industry standards and best practices.

U.S. Government Support: Potential for financial and regulatory support under U.S. critical minerals strategy with possible grants under Defense Production Act Title III program ($9 million application pending).

Market Opportunities

Growing Demand for Battery Metals: Exponential growth in electric vehicle production driving demand for nickel, cobalt, and manganese with projected battery metal supply shortages in coming years.

Supply Chain Security Concerns: Geopolitical tensions driving interest in diversified supply sources with reduced dependency on concentrated supply regions (e.g., DRC for cobalt).

Technological Opportunities

Technological Innovation: Continued advancement in collector and riser technology with improvements in autonomous underwater vehicles and remote operations.

Processing Innovations: Development of more efficient metallurgical processes for polymetallic nodules with potential for recovery of additional valuable elements.

Financial Opportunities

Access to Green Financing: Growing ESG investment pools seeking critical minerals for energy transition with potential for green bonds or sustainability-linked financing.

Valuation Upside: Current market capitalization significantly below potential resource value with re-rating potential upon regulatory approval and commercial production.

5-Year Prediction Model (2025-2030)

Model Methodology

Our 5-year prediction model is based on comprehensive analysis of company profile, historical performance, financial metrics, industry trends, and risk factors. The model presents three scenarios to account for the significant uncertainties in the deep-sea mining industry.

Key Assumptions

- Current stock price: $1.66 (as of April 1, 2025)

- No revenue generation in 2025

- Continued cash burn of approximately $55-80 million annually until commercial operations begin

- Additional financing will be secured as needed

TMC 5-Year CAGR by Scenario

Investment Return Calculator

Scenario Projections

In the baseline scenario, TMC secures regulatory approval by late 2027, with initial commercial production beginning in 2028.

| Year | Price | CAGR |

|---|---|---|

| 2025 | $1.85 | 11.4% |

| 2026 | $3.25 | 39.9% |

| 2027 | $5.80 | 51.7% |

| 2028 | $7.25 | 44.6% |

| 2029 | $10.50 | 44.6% |

| 2030 | $13.75 | 42.4% |

In the best-case scenario, TMC secures U.S. regulatory approval by mid-2026, accelerating the timeline to commercial production.

| Year | Price | CAGR |

|---|---|---|

| 2025 | $3.00 | 80.7% |

| 2026 | $6.50 | 98.5% |

| 2027 | $11.00 | 87.8% |

| 2028 | $16.50 | 77.7% |

| 2029 | $22.00 | 67.6% |

| 2030 | $30.00 | 62.0% |

In the worst-case scenario, TMC faces significant regulatory delays or denial of permits, without achieving commercial production within the 5-year timeframe.

| Year | Price | CAGR |

|---|---|---|

| 2025 | $1.10 | -33.7% |

| 2026 | $0.75 | -32.7% |

| 2027 | $0.45 | -35.4% |

| 2028 | $0.30 | -34.9% |

| 2029 | $0.25 | -31.5% |

| 2030 | $0.20 | -30.1% |

Sensitivity Analysis

The model's sensitivity to key variables demonstrates the significant impact of regulatory approval timing and metal prices on TMC's valuation:

Sensitivity Analysis: Impact on 2030 Stock Price

| Variable | Impact on 2030 Stock Price |

|---|---|

| Regulatory Approval Timing | Each year of delay reduces baseline price by approximately 40-50% |

| Metal Prices | 20% change in metal prices results in approximately 30% change in stock price |

| Production Efficiency | 10% improvement in operational efficiency increases stock price by approximately 15% |

| Capital Expenditure | 20% increase in capex reduces stock price by approximately 10% |

| Environmental Regulations | Significantly stricter regulations could reduce stock price by 25-40% |

Investment Considerations

Risk Profile

TMC represents a high-risk, high-reward investment opportunity with binary outcomes possible based on regulatory decisions. The company's success depends on multiple factors including regulatory approval, technological validation, and market conditions.

Time Horizon

A minimum 3-5 year investment horizon is recommended due to the extended timeline to commercial production. Short-term investors should be cautious given the high volatility and regulatory uncertainties.

Portfolio Allocation

Given the speculative nature, TMC should represent only a small portion of a diversified portfolio. This investment is most suitable for investors with high risk tolerance and those specifically interested in exposure to the green energy transition and critical minerals sector.

Key Milestones to Monitor

Investors should monitor these key milestones that could significantly impact TMC's stock price trajectory:

- Regulatory Developments: Progress in U.S. regulatory pathway under DSHMRA, ISA exploitation regulations adoption

- Financing Activities: Additional equity raises or debt financing, strategic investments from industry partners

- Technological Validation: Results from pilot production tests, efficiency improvements in collection system

- Commercial Agreements: Off-take agreements with end-users, strategic partnerships with equipment providers

- Market Conditions: Metal price trends, EV and battery market growth